Assessing risks: New Zealand architecture industry in 2024

BCI’s LeadManager software provides users with a database of live construction information, delivering project opportunities and company insights.

Partner Content: A group of leading New Zealand architects has cautioned that rising costs, builder insolvency and challenges linked to regulatory compliance are the primary hurdles studios will face in 2024.

The exclusive insights have come from BCI Central’s latest report, the BCI Construction Outlook, which offers valuable feedback from key market players, including builders, developers and architects.

The report unpacks and discusses the wide-ranging challenges facing New Zealand’s construction industry as well as current business focuses and anticipated work volumes across 2024.

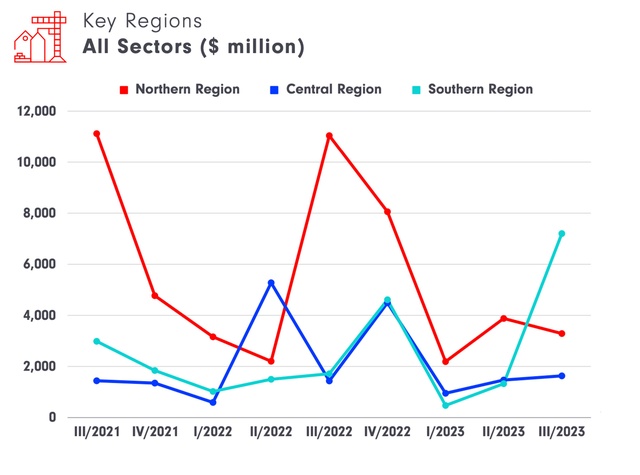

The survey insights are supported by national, regional and sector-based pipeline data trends spanning Q3 2021 to Q3 2024 — extracted from BCI platform’s LeadManager and Analytix.

Early-stage projects surge amidst sectoral dynamics

According to BCI Central, in Q3 2023, the value of early-stage projects surged by 44%, driven mainly by the industrial, infrastructure and transport sectors, contributing over 60% of the total.

The Southern Region led in early-stage project values during Q3 2023 due to significant developments in the industrial, infrastructure and transport sectors.

Over the same period, abandonment rates increased by 0.1%, while national deferral rates declined.

“The past 12 months have taught us that we need to have greater resilience as a business with a necessary cross-sector focus, migrating from mostly public projects to a good public/private sector balance,” Grimshaw Principal Katarzyna Jurkiewicz told BCI Central.

Sebastian Hamilton, Principal at Monk Mackenzie, also emphasised the industry’s susceptibility to potential risks, noting a slowdown in mid-tier developments, particularly in the townhouse range.

“The cost of funding has increased, impacting profit margins due to rising building and material prices, coupled with higher borrowing costs. This has led to stalled or halted projects,” Hamilton said.

Between Q4 2023 and Q3 2024, BCI Central predicts the industrial, infrastructure and transport sectors, as well as residential sectors, will make up 35% and 32% of project commencements, respectively.

These sectors are top contributors in the Northern Region, each representing over 30% of project values, and account for over 60% of total commencements across New Zealand.

Architects navigate existing and emerging challenges

Architects throughout New Zealand are currently contending with a complex array of challenges, including rising inflation, escalating material costs and labour shortages.

A notable 66% of surveyed New Zealand architects expressed concerns about ‘cost escalation’ while 54% flagged ‘regulations and compliance’ and 34% ‘builder insolvency’.

“The primary risk within the construction industry currently is cash flow for smaller builders as the abundance of the post-COVID years comes to an end,” Pac Studio Director, Sarosh Mulla, said.

“We have a risk management strategy within the practice and look at construction and project risk in each specific context.”

David Wingate, Managing Director of Wingates, emphasised that New Zealand, was being significantly impacted by global events and trends.

“Interest rates are a key factor as well as loan-to-equity ratios and any unforeseen issues like oil prices going up with conflicts like the Ukraine and the Israel-Gaza war,” Wingate said.

“Our focus and way of navigating this is to continue to provide quality cost-effective design solutions that provide long-term benefits. Keeping our clients happy is hugely important to us.”

James Whetter, Principal at Jasmax, said interest rates are unlikely to reduce substantially over the next 12–18 months with many property developers and investors slow to re-enter the market relying on finance.

“Those with strong balance sheets and the ability to use higher levels of equity will be able to take advantage of this and deliver good projects,” Whetter said:

“Early, integrated design processes involving the client, design, construction and cost expertise consistently deliver the best project outcomes and are a best-practice method to manage cost risk.”

Architectural practices and priorities in 2024

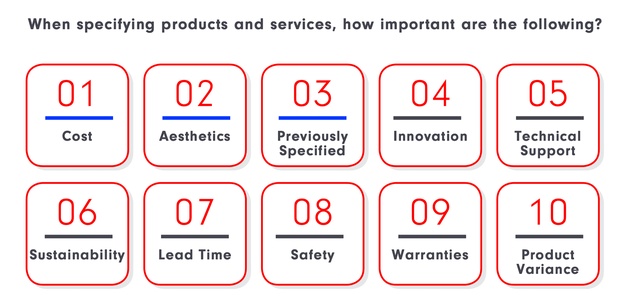

BCI surveyed studios across New Zealand to understand their design and specification practices, including factors influencing product selection and reasons for product swaps.

Over 60% use specification writing software, while just over half utilise drawing and design software such as CAD and Revit.

More than half of respondents reported that 10% to 30% of specified products are swapped for alternatives, primarily due to ‘availability’, ‘cost’ and ‘lead times’.

‘Cost’ and ‘aesthetics’ remain the most important considerations regarding product and service specifications. Notably, architects are prioritising innovation, showcasing their eagerness to actively integrate new technologies and construction methods into their plans.

‘Sustainability’ still lags in importance when specifying products and services with several interviewees stressing that ample government-led funding would be key to implementing innovative green technologies and eco-friendly building practices without financial hurdles.

“If sustainability is going to be implemented, it will be driven by two things: consumer demand, or probably more importantly, by regulation,” Moller Architects Director, Craig Moller, said.

Moller champions cross-laminated timber as a front-running solution for urban housing and climate concerns. However, for timber construction to take centre stage, both architecture and design, along with building codes, must undergo a transformative shift.

“There’s much work needed ahead to move beyond the current state of sustainability principles to achieve real regenerative outcomes with improved resilience and delivery,” WSP Principal Urban Designer, Haley Hooper, said.

Want to learn more about the current state of the New Zealand construction industry?

Download your free copy of the BCI Construction Outlook

About BCI Central

BCI Central data covers all construction sectors, including commercial, residential, education, health, legal, renewable energy, industrial, civil and infrastructure, mining, oil and gas. BCI reports on projects across Australia, New Zealand, Asia Pacific and the USA.

BCI’s flagship software, LeadManager provides users with a database of live construction project information, delivering project opportunities and company insights. Analytix uses historical construction data powered by AI to support users in understanding today’s market, identifying key players and mapping stakeholder networks. www.bcicentral.com